We’ve recently developed a 7-day-ahead electricity price forecasting tool designed for the day-ahead power markets.

Instead of directly predicting 168 hourly prices in a single step, we structured the problem differently. Electricity markets tend to operate in daily regimes, with strong intraday patterns layered on top. So we built a two-stage approach:

- First, the model estimates the expected daily price range using historical price and some other variables with effects on price behaviours.

- Second, it models the intraday structure, positioning each hour within that predicted daily range.

This separation between “daily level” and “hourly shape” helps preserve volatility and avoids excessive smoothing, which is a common issue in single-model approaches. Moreover, the framework also supports scenario analysis.

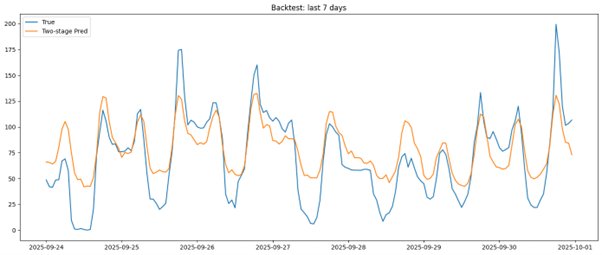

Below is a 7-day backtest comparing actual prices with the two-stage forecast. The model captures daily regimes and intraday structure consistently, with further refinement focused on improving extreme peak sensitivity.

We’re continuing to refine the model and evaluate it under different market conditions, but the architecture has proven to be structurally robust and adaptable.